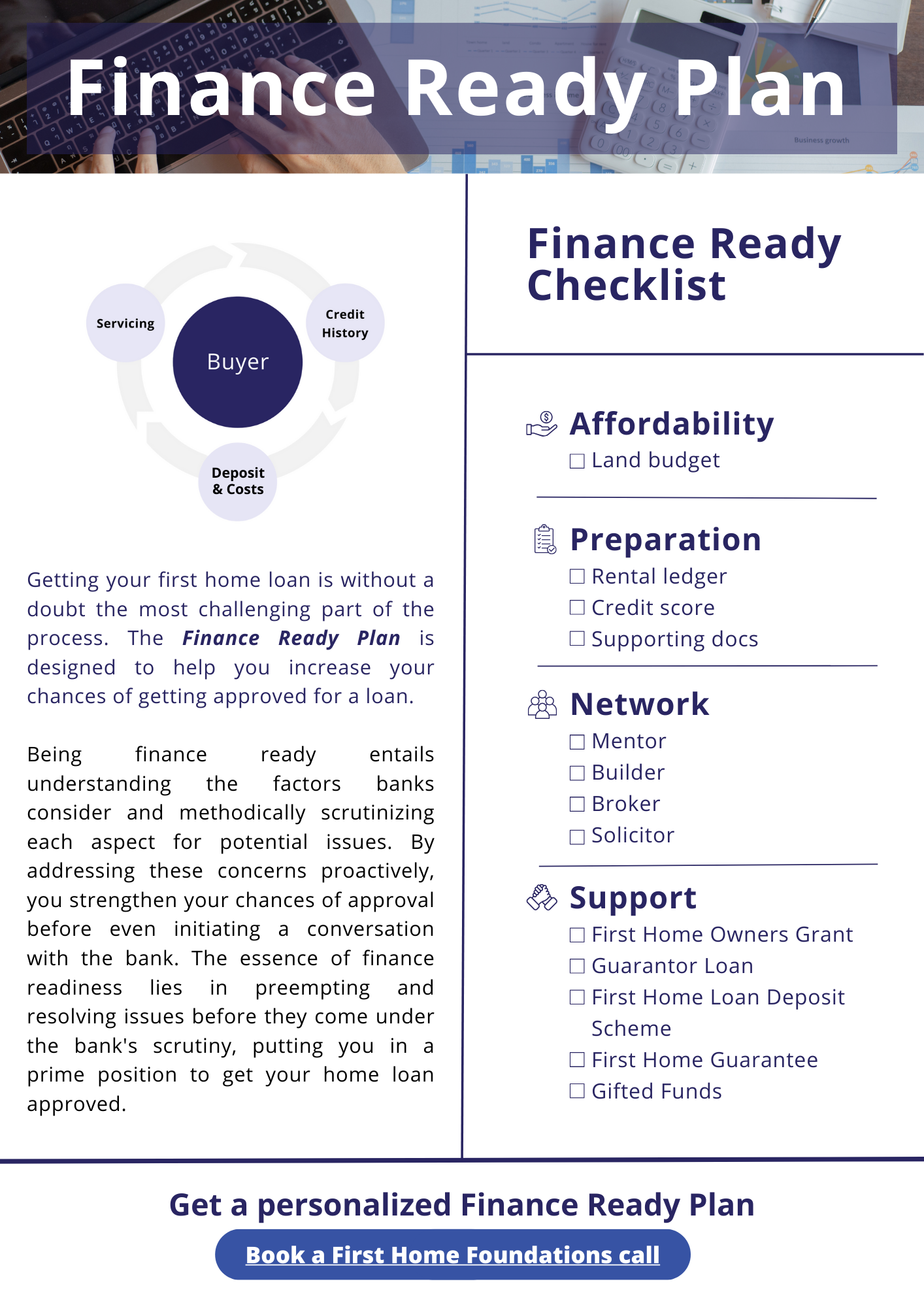

It seems a simple question to answer but believe it or not, the answer is quite complicated as deposit amounts will vary based on property prices in location, eligible grants, and your individual circumstances.

We’ve helped first home buyers to enter the property market with savings from as low as $10,000. Getting a loan from any bank means that you will need a deposit; we help to determine how much. Typically, a bank will take into account 3 major areas when assessing you for approval:

Your personal circumstances

The block of land you are purchasing

The house you intend to build on your block of land